Loss prevention departments have, for some time, successfully examined risk flags within point-of-sale (POS) transactions to identify exceptions that may indicate theft or loss. These risk flags, many of which decrease potential revenue, are increasingly categorized as SRAs or sales reducing activities. Today, monitoring SRAs to drive shrink reduction is attractive for several reasons:

- They are identifiable with analytics.

- They can be indicators for both fraud and unintentional loss.

- They are controllable through policy, procedure, and systemic changes.

- Remediation delivers ongoing profit protection.

In this article, Appriss Retail will review some common retail POS SRA events and their connection to shrink.

Common POS SRA Categories

Many activities that generate SRAs exist to improve customer service and to correct errors that occur occasionally in the normal course of conducting a sales transaction. The goal of analyzing high-level SRAs is not to eliminate all instances of the activity but rather to determine the natural frequency at which these events occur within the organization and to identify behavioral outliers from the baseline. Some SRA categories commonly seen across retail verticals are:

- Line voids and error corrects

- Post voids

- Suspends

- Coupons

- Price modifies

- Refunds

- Tender swaps

- Tax override

- Manual entries

Your retail business process may not encounter all categories, but your point-of-sale captures any SRA events and records them in the t-log. From there, exception-based reporting (EBR) solutions, like Appriss Retail’s Secure™ Analytics, can be used to analyze SRAs in detail and combine them with additional risk variables at any level within the store operational organization. Individuals with store-level responsibilities can find hotspots and resolve root causes in individual locations or request retraining for specific associates. Regional and corporate-level personnel can find and address the broader issues and causes using similar analyses for the whole organization.

An uptick in SRA frequency can indicate fraudulent activity, but when employee fraud is not found, the analyst should look for systemic or execution problems, as store employees may have developed a work-around for a problem that is not readily visible to the corporate office.

Shrink, Loss, and SRAs

Fraud—The Short-Term Concern

Even before there was a specific term, loss prevention pros monitored what we now call SRAs to find fraudulent activity. This works well when the EBR system is in the hands of a skilled user. In the course of a year, a retailer can save hundreds of thousands—even millions—of dollars and achieve excellent results by focusing on the largest cases.

Independent research by graduate students at the University of Texas at Austin showed a strong relationship between SRAs and fraud. The researchers ranked a national convenience retailer’s stores against each other for SRAs and calculated a risk factor. The 20 percent of stores with the highest risk factors were considered likely to have experienced fraudulent activity.

Systems and Processes—The Long View

A report from LP Magazine stated that in one retail chain, 77 percent of the employees who were terminated for stealing from their employers took advantage of an opportunity the employer created.

As the cost for criminal prosecution continues to rise, retailers are increasingly likely to overlook petty theft and focus only on the big cases. While a justifiable use of resources, this approach should not exclude the methodical analysis of these SRAs, which offer a better opportunity for success. By tracking SRAs and remediating the weaknesses they reveal, retailers enjoy immediate savings as well as ongoing profit protection.

Consider these scenarios:

- A retailer attempts to install a software modification to block expired coupons from being redeemed, but a software bug prevents the modification from taking place, and the coupons continue to be accepted.

- Confusion over a new employee discount policy leads to the sale of merchandise below cost.

- Professional discounts are extended to shoppers based on their appearance instead of through identification.

Those examples make it easy to understand how using SRAs to find and fix systemic problems can deliver lasting margin-protection results. As an added benefit, resolving these issues clears the clutter from transaction analysis, which makes it easier to identify employees who intended to defraud.

Seasonal Impact

SRAs and shrink trend together, and they peak during the holiday season. Research from 2016 stated that 37 percent of shrink in the US and 38 percent of shrink in the UK occurred during the fourth quarter. The SRA distribution for both countries exceeded 40 percent at that time—roughly double that of other quarters. Margins dropped by about 9 percent during this period.

One SRA in particular, returns, peaks during the fourth-quarter holiday season. According to the National Retail Federation, returns as a percent of sales were 2 percent higher than the annual rate in 2015. This tendency has been recorded for years in NRF’s annual reports.

Controlling Shrink

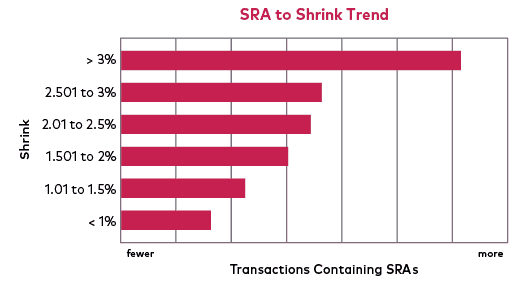

SRAs not only indicate where shrink may have taken place but also can be used as an early indicator of future shrink. By analyzing the transactions from Appriss Retail’s install base of tens of thousands of retail stores in a variety of retail verticals, the company calculated the correlation between current SRA volume and future shrink. The SRA to Shrink Trend table shows the relationship across the industry. (Results vary by individual retailer.) The more transactions containing SRAs, the higher the shrink percentage. Therefore, reducing SRAs will help reduce shrink.

The table clearly shows the correlation of SRAs and shrink. By monitoring SRAs throughout the year, retailers can detect problem stores and resolve root causes before it is too late.

Erosion of Net Sales

The errors or other situations that instigate legitimate POS SRAs diminish the customer experience for everyone waiting to check out—whether it is a pricing error that leads to a line void, the need to adjust tax for a professional contractor, suspending a sale while the consumer returns to the car for a wallet, or any number of other issues slow transaction times. The flow chart above right shows some of the common impacts.

Monitoring SRAs for Improved Financial Performance

Both “good” and “bad” SRAs impact shrink. They should be monitored on a corporate level to identify emerging problems quickly, before annual shrink is calculated. In addition, people with store and regional responsibilities can use them to spot unusual activities at store level. An LP professional, for example, will make better use of the time spent on a store audit by running an SRA report in advance.

Analyzing the SRAs with Appriss Retail’s Secure Analytics is a quick and effective way to learn where to focus efforts to reduce shrink and ultimately improve profits. Visit apprissretail.com for more information.